Drive Shack Continues to Bet Big on Puttery

But their driving range business is beginning to slip.

Every Monday, I write a newsletter breaking down the business in golf. Welcome to the 57 new Perfect Putt members who have joined us since last Monday. Join 3,987 intelligent and curious golfers by subscribing below.

Hey Golfers —

Drive Shack reported second-quarter earnings on August 9th. They reported decent numbers — beating top-line revenue expectations by 5% and earnings per share expectations by 52%.

While a company’s share price isn’t necessarily an indicator of success or failure — I couldn’t help but notice the stock is down 11% in the last five days and down 46% in the last year.

For context — here are public companies Callaway and Acushnet returns over the same period. As well as the S&P 500.

Callaway 5 day — up 4%

Callaway 1 year — down 18%

Acushnet 5 day — up 5%

Acushnet 1 year — down 2%

S&P 500 5 day — up 3%

S&P 500 1 year — down 4%

Drive Shack has beat top-line and bottom-line expectations in the last four quarters, yet they have lost nearly half their market cap in the last year. This begs the question — is Drive Shack in trouble?

I’m not sure we know the answer to that question — but let’s outline what we know.

A quick recap and background on Drive Shack.

Drive Shack has three business units.

Puttery

Drive Shack

American Golf

Drive Shack was once known as Newcastle Investment Corp. In 2013 — Newcastle Investment Corp acquired American Golf. American Golf owns and operates golf courses — similar to Invited (ClubCorp) on a smaller scale.

In 2017 Newcastle Investment Corp changed its name to Drive Shack. In parallel with the name change — they moved from a REIT to a C-Corp and began the transformation to a leisure company.

The strategy was to move into golf entertainment — and build out the Drive Shack business unit — a Topgolf competitor.

Drive Shack had big plans in 2017 — they announced five locations in the pipeline and would self-fund the transformation with the $182 million in cash on hand.

It is always easy critiquing business decisions in hindsight. Going up against Topgolf, who had over 30 venues in 2017 and a clear first-mover advantage, was going to be incredibly tough.

Drive Shack opened one venue in 2018 and three in 2019 — they haven’t opened a new location since. Drive Shack fully exited their plans to build a venue in New Orleans and recently terminated its lease at a loss. They currently have one venue in the pipeline in New York City. It is fair to wonder if that venue will eventually open.

Here is the concerning thing with Drive Shack venues — they aren’t growing revenue, and their EBITDA margin is declining. Drive Shack venue revenue was down 3.5% in the second quarter, and their EBITDA margin was down 17% in the quarter. For context — Topgolf's same venue revenue grew 8% in the second quarter.

We know the golf entertainment space is growing — so why the decline? Could it be a lack of focus on the Drive Shack business unit?

It is evident that Drive Shack is making a full pivot to Puttery.

And I generally agree with the business thesis of Puttery.

It’s low cost

Quick to market

First-mover advantage

Requires fewer square feet

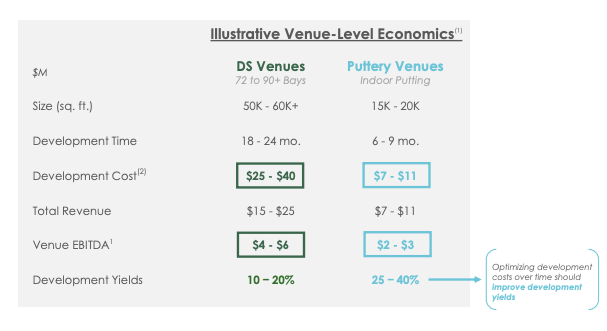

This graphic summarizes it well.

Puttery recently opened its third location in Washington, DC.

They have four venue openings in the pipeline for the remainder of the year.

Houston

Chicago

Pittsburgh

Kansas City

Charlotte and The Colony have performed in line with Drive Shack's expectations. Both venues are on pace to bring in around $3 million in EBITDA for the year. The EBITDA margin is healthy at 29%.

But Drive Shack has an issue — Cash. They have $22 million on hand compared to the $58 million they had on hand at the end of 2021.

Puttery venues require $7 - $11 million to build. To fund the Puttery pipeline Drive Shack will need to sell some of its assets, likely from its American Golf portfolio, and finance it with debt.

Puttery generates cash — but Drive Shack needs more cash to scale the business properly. Or they risk losing their first-mover advantage to competitors entering the space, specifically Puttshack.

Drive Shack deserves some credit.

Drive Shack transformed its business from a REIT to an entertainment driving range to entertainment mini-golf in five years. Business transformations require corporate culture shifts — something understated going through the process.

I am pulling for Drive Shack’s success — the next 6 - 12 months will provide a good idea of how the business will shake out.

Have yourself a great Monday. Talk to you next week!

Your feedback helps improve Perfect Putt. How did you like this week's newsletter?

If you enjoyed this week’s newsletter, please share it with your friends :)

Are you interested in partnering with Perfect Putt? Click the button to learn more about sponsorship opportunities.