FOX Paid $320 Million to the USGA

The details behind the contract breakup and the financial ramifications to the USGA.

Every Monday, I write a newsletter breaking down the business in golf. Welcome to the 114 new Perfect Putt members who have joined us since last Monday. Join 3,336 intelligent and curious golfers by subscribing below.

Quick housekeeping note: My wife is scheduled for a C-section this week. Next week’s newsletter will be from a guest writer!

Hey Golfers —

FOX announced a 12-year contract with the USGA in 2013 valued at $1.1 billion — $93 million per year. NBC and ESPN had the prior contract; combined, it was $37 million per year. FOX’s TV deal with the USGA represented a 150% increase from the preceding contract.

A few years later, in 2016, there were reports FOX and the USGA weren’t happy with the deal.

FOX lost money the first two years

The USGA didn’t appreciate how some of their events were covered

And both issues made sense for each party.

The U.S. Open generates nearly all of the USGA’s revenue and is the only USGA event that makes a profit (this could change in 2022 with the U.S. Women’s Open and their sponsor, ProMedica). While FOX’s TV contract included 13 USGA events, the deal was essentially for the U.S. Open.

FOX had never televised golf before signing the USGA contract. It was reasonable to think the coverage would be choppy, and there would be some errors on FOX’s side of covering USGA events.

These issues laid the groundwork for a contract situation.

How did the USGA receive a $320 million payout from FOX?

The 2020 U.S. Open was moved to September due to COVID-19. FOX could not cover the event with its NFL, MLB, and college football commitments on its schedule.

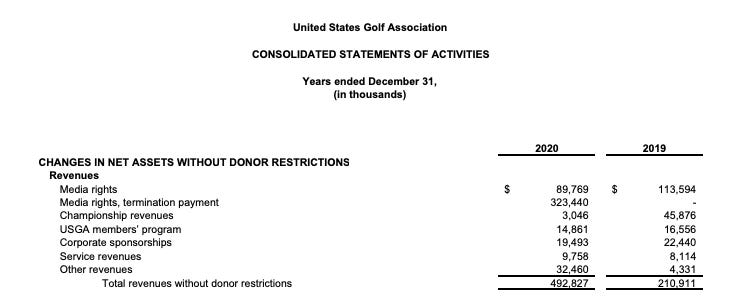

FOX and the USGA parted ways, and NBCUniversal assumed the contract from FOX for the same duration — until December 31st, 2026. While the contract's financial details were confidential, the USGA’s financial statement from 2020 states the below.

The new contract with NBCU was at a lower value than that of the original FOX agreement, and as a result, FOX paid the USGA a lump-sum representing the present value of the remaining fees due under the original contract less the amounts to be paid by NBCU. In addition, the deferred portion of the original FOX signing bonus was accelerated and recognized in 2020.

FOX paid the USGA $323.4 million to terminate the contract.

The USGA recognized nearly half a billion in revenue in 2020, thanks to the termination payment.

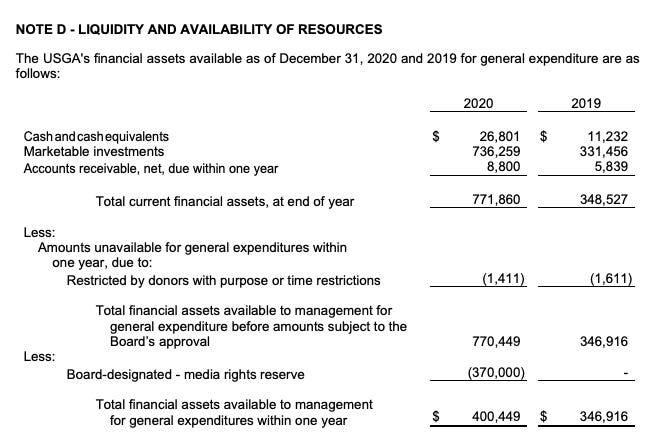

While the cash from the termination payment looks good on the financial statements — the USGA Executive Committee formed a board-designated media rights reserve for $370 million. Each calendar year, the USGA may release into operations an amount, which, together with the NBCU revenue, will approximate the annual domestic media rights revenues that would have resulted from the FOX contract. Meaning the USGA will dump an additional ~$30 million into its operation each year to make up for the contract difference.

Here is a quick breakdown of 2020 USGA financial assets.

The significant difference in marketable investments from 2020 to 2019 leads me to believe that a good portion of the termination payment from FOX has been allocated to this account.

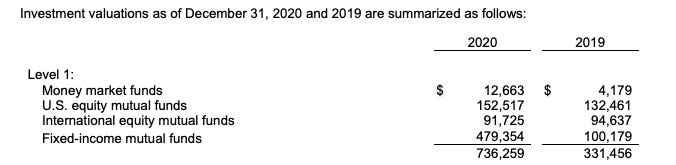

Here is a breakdown of the USGA’s marketable investments.

It makes sense the USGA invested the termination payment money to create a return.

Let’s take a look at a couple of scenarios.

Mutual fund returns

Fixed-income returns

At the end of 2020, the USGA had $243 million invested in mutual funds — U.S. equity and International equity. The S&P 500 has returned an average of 10.5% annually since its inception in 1957. In theory — the USGA could expect a return of nearly $25 million per year.

Here are the S&P 500 returns for the last two years as a baseline.

2021 — 26.9%

2022 (YTD) — (18.7%)

Even with the S&P 500 down nearly 19% in 2022 — the $243 million has remained positive for the USGA (assuming those mutual funds mimic the S&P 500 and no investment changes were made).

Since the fixed-income mutual funds show a difference of $380 million — the most likely place where the USGA allocated the FOX termination payment, let’s look at this scenario.

At the end of 2020, the USGA had $480 million in this account. Generally speaking, fixed-income mutual funds are a low-risk, low-return product compared to an S&P 500 mimic mutual fund.

From 1926 - 2019 the average annual return for a 100% fixed income fund was 5.3%.

Here is a look at the performance of a Vanguard fixed-income mutual fund.

2021 — (2%)

2022 (YTD) — (12%)

Not an ideal return for the last 18 months for the $480 million.

If the USGA received the historical average of 5.3% — the USGA could expect a return of $25 million per year.

Looking at pre-COVID in 2019 — the USGA’s expenses were $199 million. FOX’s termination payment could cover 12% of the USGA’s budget off the return, based on an average year in the market. This assumes that the USGA allocated the termination payment money to fixed-income mutual funds.

Adding those two investment categories together — in an average market year, the USGA would see a return of $50 million on its assets. Enough to fund 25% of its expenses.

Quick numbers from the USGA’s financial statements in 2020.

$492 million in revenue

$176 million in expenses

$736 million in investments

Looking at a baseline from the PGA Tour’s 990 in 2019.

$1.41 billion in revenue

$1.34 billion in expenses

$2.44 billion in investments

All items considered, the USGA is an extremely healthy organization from a financial perspective.

Here is a quick fun fact from the USGA’s financial statement.

GHIN and handicap revenue was $7.4 million in 2020, an increase of 41% in 2019.

Enjoy the U.S. Open — the best golf tournament of the year!

Have yourself a great Monday. Talk to you in a couple of weeks!

Your feedback helps improve Perfect Putt. How did you like this week's newsletter?

If you enjoyed this week’s newsletter, please share it with your friends :)

Are you interested in partnering with Perfect Putt? Click the button to learn more about sponsorship opportunities.

Great piece as always!

One might reasonably ask why the USGA insists on becoming wealthier and wealthier when their mandate (backed by a US tax exemption) is to be the national governing body for golf. The blue blazer crowd incessantly solicits golfers for donations ("for the good of the game"). They might want to spend some of their time, energy and money showing us what they're putting back into golf. (NOTE the only reason the US Women's Open purse jumped was because Pro Medica came on board, not because Far Hills wanted to give the women's game a shot in the arm.)